Retirement is one of those things that should be taught in a classroom. It’s something that most people tend to ignore until their later years, and that’s a shame, but it’s never too late to start planning. You just need to know your options.

Today, we’re going to talk about the most effective ways to save for your retirement.

Start in Your 20s

First off, we need to make something clear right now. If you are in your 20’s or even a little younger and starting your first job, don’t think that retirement is something that you don’t have to worry about.

Yes, you could wait 10 or 15 years to get started, but the numbers look much better when you start early.

| Age | How Much You’ll Have for Retirement |

| Let’s say that you’ve decided to put off investing in your retirement until the age of 35. At 35 years old, you elect to start putting $100 per month into your retirement account. | Okay, great! Let’s fast-forward 30 years now. At the age of 65, with compound interest roughly factored in, you’ll have a rounded amount of roughly $150,000. |

| Now let’s see what happens if we start earlier. If you decide at 25 years of age to pay only $75 a month. | When we hop into our time machine, we find that 65-year-old you now has a whopping $264, 600. |

Starting early means that you can pay less now and keep paying less, while still realizing a substantial difference.

Imagine what happens if you change that $75 to $100 a decade or two down the line… It doesn’t seem like much, but investing now really makes a huge difference over time.

Understand Inflation

When you were a kid and you got thirsty, you’ll surely remember popping into the store to buy yourself a soda.

Assuming that you are 27 years old, a can of Coca-Cola in 1994 cost you about 75 cents, but as of 2020, that same can would cost you about $1.20.

![]()

That’s an average inflation rate of 1.71% per year and sodas, sadly, are on the LOW side of inflation. Now that $150k vs. $264k is a lot more troubling.

Prices are going to change and the sooner that this sinks in, the better.

While it’s an uncomfortable truth, realizing now how inflation can affect your golden years is a great motivator to start saving NOW for your retirement.

Set Up Direct Deposit

So, how should you get started? The easiest way to save is to set up your direct deposit. This will allow you to automatically send money to your savings account or a 401k account (which is much better, as we’ll discuss shortly).

If you do this as soon as you start a new job, you won’t miss the money.

If you’ve already been working for a while, set up your direct deposit anyway.

After a little time passes, you won’t miss the amounts that are going to your savings, and you’ll be amazed how quickly those small amounts build up over time.

Financial Advisors Are Useful

Many of us don’t take advantage of good opportunities because they tend to be a little confusing. When your job tells you about various investment and retirement plans, the language involved includes a lot of numbers and projections…. It’s kind of overwhelming.

This is where a financial advisor is a good idea.

A lot of people think that financial advisors are just for rich people and that they are just there to try to sell you stocks and to get your money.

Nothing could be further from the truth. Financial advisors are professionals who are educated in ways to SAVE you the most money—read more from CNBC.

Even if you don’t have a lot of assets right now, a single consultation can make you aware of options you might not even know that you had. Your advisor can translate all of the fine print and do the math for you to explain your options in simple terms.

Best of all, you might only need that one consult and nothing more from them until 10 more years down the line! Do yourself a favor and take our word for it.

One single visit to a Financial Advisor can make an enormous difference in your eventual spending power and your retirement.

Married? Plan Together

If you are married, just like you would plan a house purchase together or start a business together, retirement is something that you can and should talk about to increase your options for when you both retire.

If you and your spouse are both contributing to an eventual retirement then it’s easy to keep each other on track. And when the time comes to leave the rat race and start enjoying the rest of your lives together, you’ll have a lot more power over your retirement

Your 401(k) Is More Powerful Than You Think

If your job offers a 401(k) and you aren’t contributing to it, you are shooting yourself in the foot. 401(k) plans are amazing and they often come with incentives that can benefit you as the years go by – even before your retirement.

First off, when you contribute to your 401(k), it is pre-tax. That means if you are contributing say $75 from a $1,000 paycheck, then you won’t get taxed on that $75. Instead, you’ll get taxed on the remaining $925 as normal. This can be an enormous benefit, especially if you are approaching a higher tax bracket.

By putting away extra money in retirement, when your yearly taxes get assessed, if you’ve put away enough to keep you in the lower tax bracket then you get to keep the extra money that you have earned. So the next time you get a raise, consider raising the amount you put in your 401(k) just for this alone.

The savings can be quite amazing!

Employer Matching Plans | Don’t Lose Free Money

Many employers offer to match 401(k) contributions up to a certain amount.

If your employer does this, then don’t miss the boat. Contribute the maximum amount that they will match. If you don’t, you are literally turning down free money.

401(k) Loans

If you are worried about emergencies or saving up to start a business, check out the terms of your 401(k) plan now.

Savings accounts are nice, but some 401(k) plans will let you borrow against your 401(k) and you get an amazingly low interest rate that is especially good if you have less-than-stellar credit.

If your plan includes this, by saving for your retirement in your 401(k), you also empower yourself to get low interest loans for hard times or for starting that business that you’ve been thinking about for years.

Best of all, instead of borrowing from someone else, you’re just borrowing from yourself.

Your 401(k) thus is a way to not only prepare for your retirement, but it will slowly increase your financial power over the years and this is a valuable thing indeed.

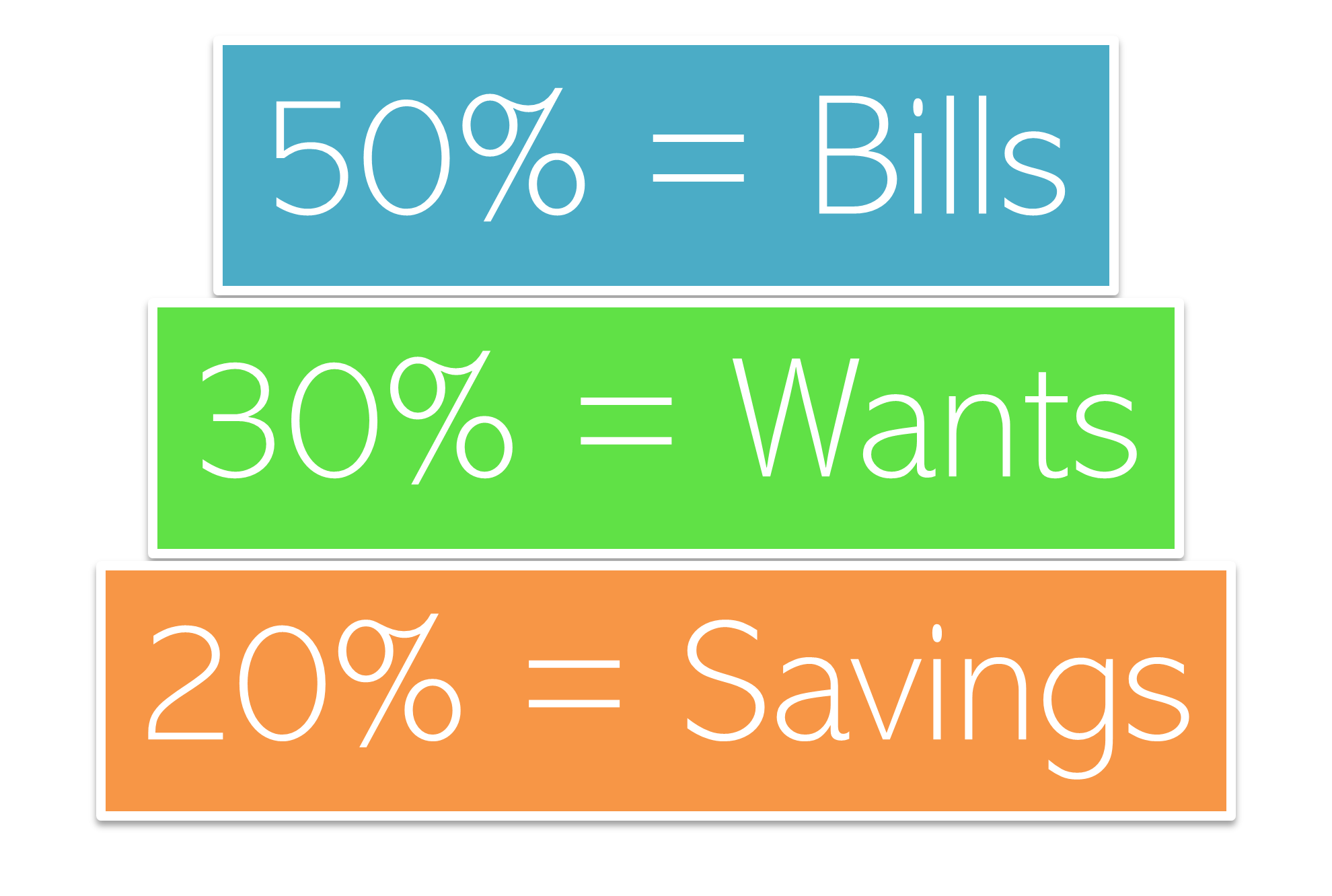

The 50/30/20 Rule | Learn It and Live It

The best way to save for your retirement is also one of the hardest, but if you can master this rule now then you’ve got an amazing future waiting for you on the horizon. The 50/30/20 rule seems pretty basic, but it can make a huge difference.

- 50% of your income is what you will spend on things that you NEED. This includes rent, utilities, groceries… just the necessities.

- 30% of your income is for things that you want. This might be a new phone, a laptop, that Netflix subscription… you get the idea.

- 20% should always go to savings or investments.

If you can discipline yourself to follow this rule, you’re going to have a world of financial options that your friends and coworkers simply won’t have.

Final Thoughts

As you can see, the best option is starting early but that certainly isn’t the only option. Think about inflation, make your plans, and set your direct deposit up to help to keep yourself on track. If you are married, plan together with your spouse – it will make an enormous difference.

Invest in your 401k and always contribute as much as your employer will match. Finally, if you can master the toughest rule on this list – the 50/30/20 – then you can rest assured that your golden years are going to be golden indeed!

There aren’t a lot of things that we can control in life, but retirement doesn’t have to be one of them. Start taking charge of yours now!

To read more on topics like this, check out the Lifestyle & Goals category

Leave a Reply